When financial services and public digitisation go hand in hand

Denmark's journey in financial digital services is a blend of innovation, trust, and collaboration. The country's success is driven by a proactive approach to technology, digitalisation, and an evolving financial sector that serves both consumers and businesses.

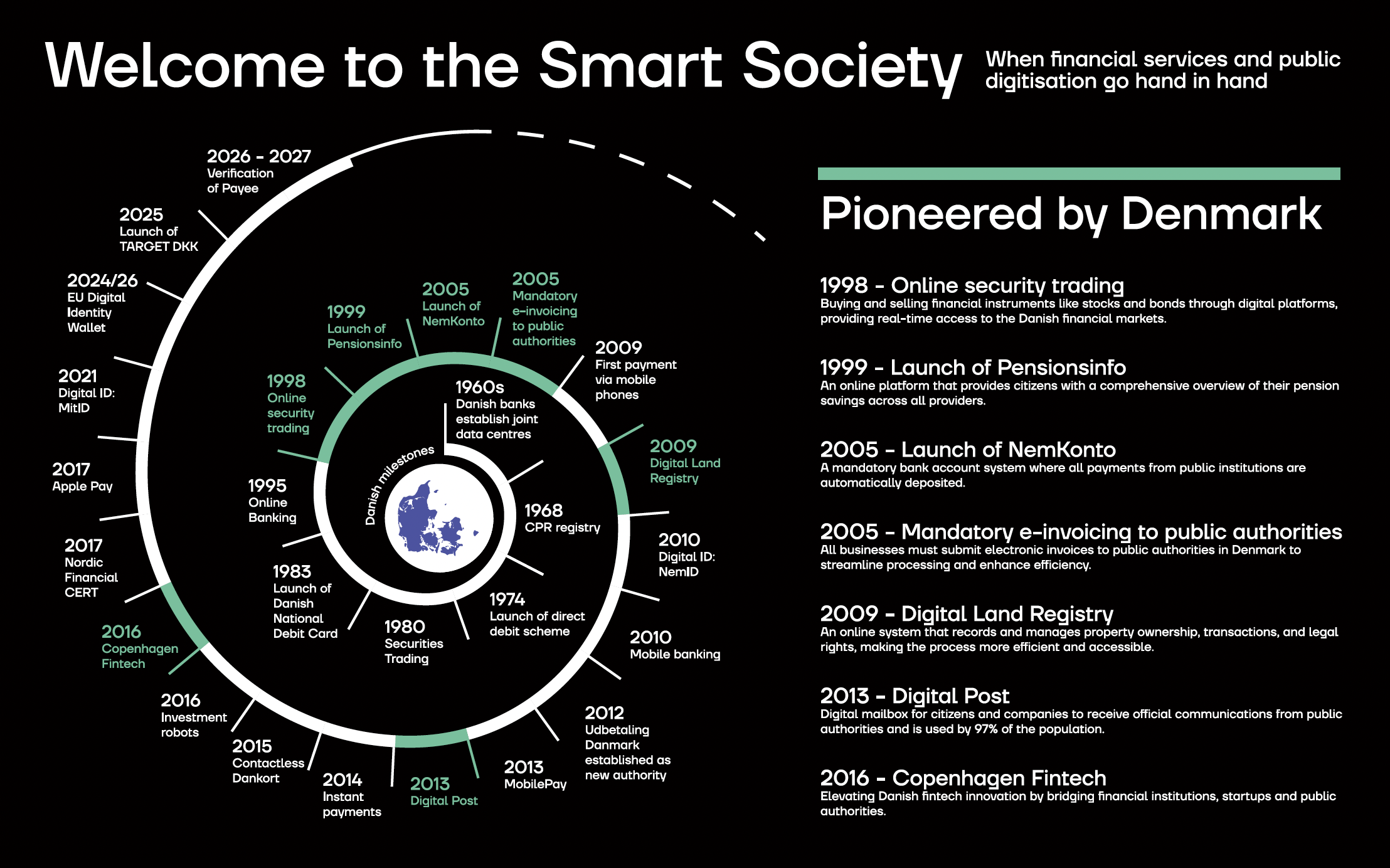

A key factor in this success has been the strong collaboration between banks and the public sector, which dates back to the 1960s. This early partnership laid the foundation for Denmark’s digital financial infrastructure.

A Strong Foundation

Denmark’s financial system has long been characterised by stability and efficiency, but it was in the mid 1990s that the country truly embraced digital services. Banks were among the early adopters of technology, introducing online banking platforms in 1995 that gave Danes easy access to their financial accounts.

As a country with a small, yet tech-savvy population, Denmark was able to develop a solid infrastructure to support these advancements. The first national digital strategy was launched in 1999, and the widespread adoption of broadband internet during this time was another factor that facilitated Denmark’s financial digital transformation.

One of the most important milestones in Denmark's digital financial services space was the launch of NemID in 2010. NemID is a national digital signature and authentication system that allows citizens to access financial services and a range of government services securely. This centralised digital identity has fostered trust in online financial transactions.

With NemID, Danish citizens could safely access their bank accounts, pay bills, transfer money, and even manage pensions from anywhere. The system was widely adopted across banks, and its integration into government services meant that users only needed one digital identity for almost everything. The high level of trust in the government and financial institutions made Danes some of Europe's most frequent online banking users.

A testament to the benefits of close partnership between the public and private sector is the Digital Land Registry, a groundbreaking initiative that streamlined property transactions, making them more efficient, transparent, and secure.

In 2013, Danske Bank launched MobilePay, quickly becoming a game-changer in the Danish digital financial ecosystem. This peer-to-peer (P2P) mobile payment app allowed users to send money to friends, pay for goods and services, and simply donate by linking their phone numbers to their bank accounts. MobilePay spread rapidly across Denmark, becoming one of the most used payment methods in the country.

The ease of use, security, and convenience of MobilePay made cash and even card payments less necessary for daily transactions. It was adopted by people across all age groups, from teenagers splitting bills to seniors making donations. Merchants and small businesses also embraced MobilePay, integrating it as a key method of accepting payments.

MobilePay's success laid the groundwork for a growing digital payment culture in Denmark, with many other Nordic countries following suit. The rise of digital payments accelerated the country's transition toward a cashless society.

FinTech startups also began to thrive in Denmark, supported by venture capital, government programs, and collaborations with traditional banks. Companies like Lunar, a challenger bank, and Pleo, a digital expense management service for businesses, emerged as major players. These startups introduced innovative financial products that cater to a new generation of consumers and businesses that demand convenience, transparency, and flexibility.

In 2016, Copenhagen Fintech was founded to create a collaborative environment where startups, financial institutions, regulators, and investors can connect and drive the growth of fintech in Denmark. Its mission is to foster innovation, collaboration, and entrepreneurship in the financial technology space, not only in Denmark but across the Nordic region and globally.

In 2018, Denmark, in line with the rest of the European Union, adopted the Revised Payment Services Directive (PSD2). This regulation required banks to open their data to third-party providers, enabling more competition and innovation in financial services. Danish banks embraced this change by partnering with FinTech firms to offer more tailored services. As a result, customers gained better access to various financial products, often through one digital platform.

Open Banking has also contributed to the rise of personal finance management apps that allow users to view all their accounts in one place, automate savings, and receive personalised investment advice. This has created a more dynamic and customer-centric financial ecosystem in Denmark.

By 2021, Denmark introduced MitID, the successor to NemID, further modernising the country’s digital identity infrastructure. MitID is more secure and future-proof, providing stronger authentication methods, particularly in a world where cyber threats are rising. The seamless transition from NemID to MitID ensured the country maintained its digital momentum while improving security standards.

Today, Denmark is one of the most digitised countries in Europe regarding financial services. Around 90 per cent of Danes use digital banking, and physical cash is becoming increasingly rare daily. With mobile payments, contactless cards, and digital wallets integrated into daily routines, Denmark is well on its way to becoming a cashless society. The government's encouragement of digital services, combined with a tech-savvy population and innovative financial players, has cemented Denmark's position as a global digital finance leader.

While Denmark has made incredible strides, challenges lie ahead. Cybersecurity is a growing concern, with cyberattacks becoming increasingly sophisticated. As Denmark pushes toward further digitisation, ensuring the privacy and security of its financial system remains a priority.

Another challenge is financial inclusion. Even though digital services have permeated most parts of Danish society, some groups—such as the elderly or those without access to digital devices—may struggle with the rapid pace of change. The Danish government and financial institutions continue to work on bridging these gaps to ensure that no one is left behind.